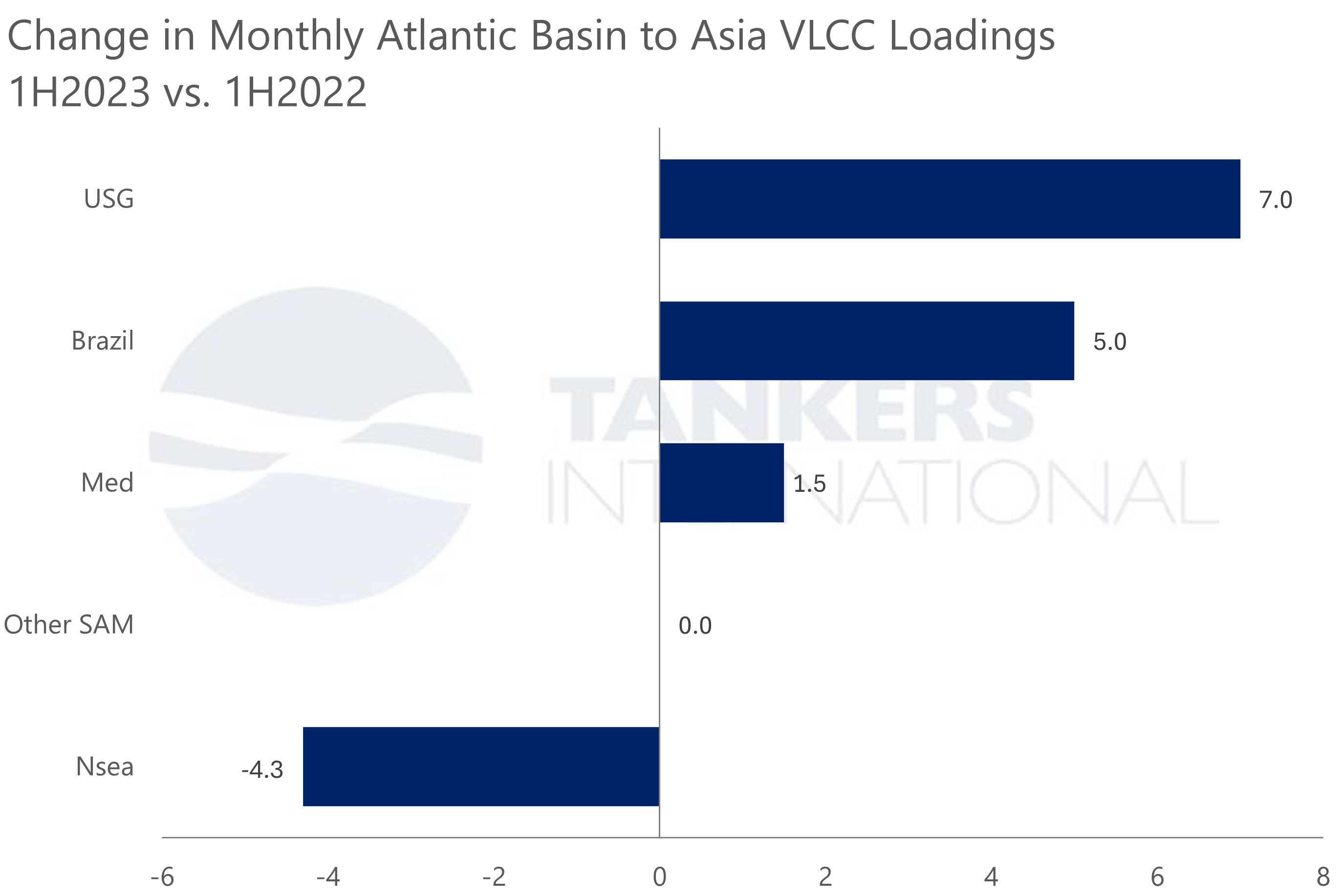

The Atlantic basin is providing massive support for the VLCC tanker market. Growing supply from the region means long tonne-miles across the Atlantic as much of the oil is being shipped to the Far East. In the Far East, we continue to see demand from China ramping up after COVID lockdowns. While the market’s expectations for China were perhaps too optimistic to begin with, we are still seeing signs of recovery, and oil demand remains healthy and likely to improve progressively. Furthermore, despite weaker economic data and somewhat depressed market sentiment in recent weeks, major reporting agencies have not made significant downward revisions to oil demand forecasts yet.

Low vessel supply growth is adding to the good news for shipowners. Despite an ageing fleet, shipowners remain reluctant to place newbuild orders, with not a single VLCC to be delivered in 2024 and only one ship in 2025 and one in 2026.

This shortage in newbuilds is allowing market fundamentals to rebalance after the massive drop in demand of the COVID years. Even the production cuts announced by OPEC+ nations such as Saudi Arabia have not dampened the mood. Rather, the capped volumes are expected to be filled by producers such as Brazil, resulting in more long tonne-miles for VLCCs across the Atlantic to Asia. The Chinese market is huge and is one of the key drivers of the VLCC market, and the resumption of trade there is countering other market concerns.

Historically in the freight market, we have seen VLCC rates putting pressure on Suezmax rates, which have then put pressure on Aframax rates. However, since the invasion of Ukraine, this trend has largely reversed. Aframax and Suezmax rates spiked initially when some owners took the risk of shipping Russian crude. As freight levels in the smaller tanker segments rose to historical highs, the VLCC segment became competitive in markets that it has not traditionally traded in, such as West Africa and US Gulf to European destinations. This has given VLCC owners optionality. They can choose to keep their vessels local in the West or trade them longer-haul on the traditional routes to Asia, depending on their views on the freight market.

The VLCC market has been seasonal in the past, with high rates in winter and lower rates in summer. However, this pattern has weakened over the last few years, and this year in particular, we are experiencing sound second-quarter results that have kept the market buoyant amidst the borderline recession in some parts of the world and the lingering macro-economic effects of the pandemic.

In 2023, Brazil introduced a new freight tax, which caused oil exports to drop dramatically. Oil companies reduced or halted their VLCC export programmes rather than paying the additional costs. This decision appears to have coincided with an increase in West African VLCC fixtures to meet part of the demand, particularly from China, with West African fixtures in June increasing by at least 50% month-on-month.

The demand for high oil volumes from Africa over long tonne-miles to China has been good news for VLCCs. The oil export tax in Brazil is due to end in July, and the Brazilian market is likely to resume, and while this may remove some VLCC trade from West Africa, it is still long tonne-miles for VLCCs.

The prominence of the Atlantic basin trade for VLCCs is therefore set to continue to keep shipowners smiling well into the next quarter.