As we wrap up the first quarter of 2024, the VLCC freight market continues its upward trend amid rising tension in the Bab-el-Mandeb, tightening of sanctions on companies involved in Russian oil trade, and the OPEC+ group announcing an extension of the supply curbs that were put in place at the start of the year. Yet, with Baltic freight assessments and sentiment improving, the VLCC market is on the up. So, how have these developments impacted the VLCC market, and what is the outlook for the next quarter?

While the crude tanker market looks set to face a slowdown in global oil demand growth, the outlook for growth in 2024 remains in line with what we have seen in previous years, and the outlook for the year keeps improving. This is reflected in the IEA forecasting an additional 1.3 million barrels of growth in 2024, which matches the average between 2000-2019. We also need to remember that the fast-paced demand growth we experienced in the last couple of years was the market playing ‘catch up’ following the demand destruction of the Covid years. Demand growth will be driven by economies in the Far East, with China and India leading the way.

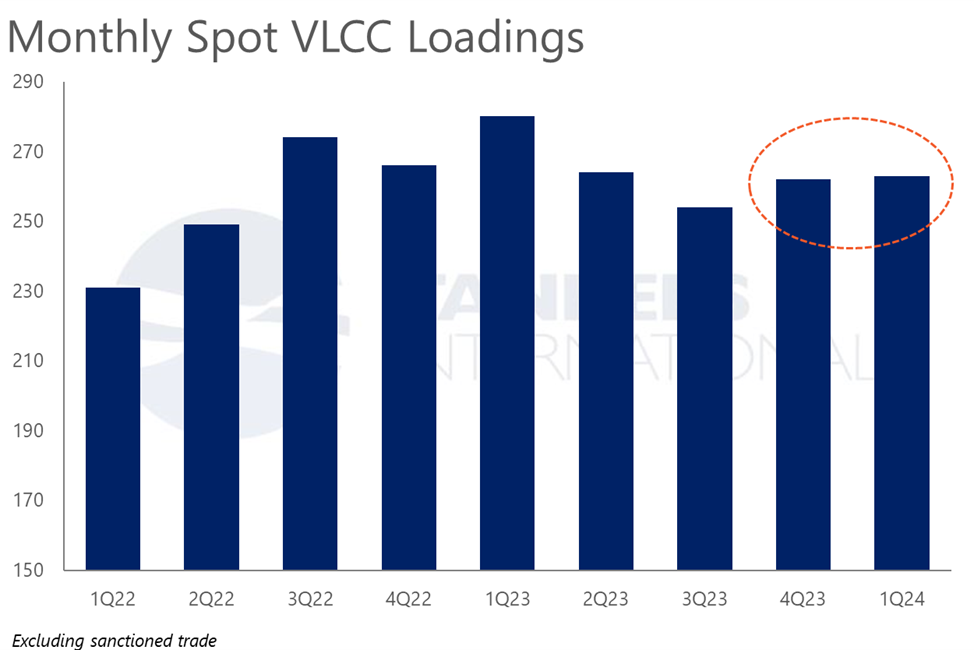

The OPEC+ alliance is also driving oil headlines by announcing a voluntary tightening of supply going into 2024 and a further declaration to extend the production curbs into the second quarter. There have been reports of lax quota compliance from some alliance members, and the voluntary nature of the production cuts supports this theory. Meanwhile, producers in the Atlantic basin are set to continue to add incremental supply and this will compensate for some of the tightening of supply from OPEC+ alliance, and will satisfy the demand gap in the Far East. Preliminary data from our VLCC fixture database, does not show any significant drop in fixture volume, and this is across all the major load regions.

The escalation of the tension in the Bab-el-Mandeb strait through the first quarter, with further attacks on oil tankers, has seen a significant decline in international tonnage of all types transiting the strait and the Suez Canal. The alternative trade route via the Cape of Good Hope adds considerable tonnemile to the oil trade, and there is no sign that this will change in the near future. Looking specifically at the VLCC segment and the 6-8 monthly liftings from the Middle East to Europe that historically have passed the conflict area, the majority of owners and charterers are now opting for the longer, safer transit route via the Cape. This adds around 15 days to the laden leg of the voyage, and apart from delaying crude supplies reaching Europe, it also increases tonnemile demand for the VLCC segment.

The start of this year has also seen tighter enforcement of Russian sanctions, and this threatens to once again transform the commercial framework around the trading of Russian oil. The Russian market is becoming increasingly difficult for mainstream industry players to get involved with and Russia continues to rely on the dark fleet to move its barrels. Only a few VLCCs are involved in lifting Russian cargo, and the commercial implication for our segments remains with the shift in general trade flows whereby Europe is taking more crude from the Atlantic Basin, and from the Middle East.

One of the biggest stories from this quarter has been a resurgence in VLCC tonnage ordering. The first three months of the year saw the orderbook double in size, and historically an expansion of this scale would pose a huge disruption to the freight market outlook. However, the orderbook-to-fleet ratio remains historically low even with the addition to the orderbook. The full orderbook holds 51 orders to be delivered over the next five years, equivalent to 6% of the fleet. But this compares to an ageing fleet profile of more than 200 vessels that will reach the age of 20 or older within the same time period. This means the potential for fleet exits by far exceeds additions.

Looking ahead into Q2 and beyond, the VLCC freight market looks set to continue to build on the solid foundation of cargo volumes that has persisted from last year and into this year. Recent headlines also point to both China and the US – the world’s biggest oil consuming nations – signalling the need for more oil than expected this year, driven by rising manufacturing activity and stronger-than-expected economic conditions. There is further upside ahead if the OPEC+ alliance begins to unwind production cuts, which many analysts and forecasting agencies see as a likely scenario going into the latter part of the year. Until then, the geographical mismatch between where oil demand is growing and where new supply will arise will continue to add to the tonnemile equation and to the demand for VLCC tonnage.