This year marks Tankers International’s 25th anniversary, a quarter of a century since the launch of the world’s leading VLCC pool, backed by some of the world’s leading ship owners. During that time, the crude tanker market has experienced profound change.

From regulatory shifts and shipbuilding cycles to evolving trade routes, new customer profiles, geopolitical shifts, and the rise of data-driven decision-making, the market we operate in today looks almost unrecognisable compared to 2000, when the TI Pool started operating. However, amidst all these changes, one constant remains, the vital role of VLCCs in powering global trade and meeting the world’s energy needs.

As we celebrate this significant milestone, it’s worth reflecting on the ‘then and now’ to explore just how dramatically the industry has changed.

Regulation: From double hulls to decarbonisation

In the early 2000s, the industry was adapting to the Oil Pollution Act of 1990 (OPA90), which phased out single-hull tankers in favour of more secure, double-hull designs. This sparked a wave of newbuilding orders and set higher safety and environmental standards across the tanker fleet.

Fast-forward two decades and the focus has shifted from structural safety to emissions reduction. The IMO 2020 sulphur cap, effective from January 1st, 2020, established a global sulphur cap of 0.5% on marine fuels. This forced shipowners to make a strategic choice; to run vessels on more expensive low sulphur fuel oil, to retrofit existing vessels with scrubbers or to invest in new, compliant tonnage.

As a result, new ship designs increasingly featured scrubber systems built into their propulsion setups to ensure compliance from the outset of the new regulation.

Today, the innovation drive continues for shipowners, but the focus has shifted towards adopting alternative, lower-emission fuels such as LNG, ammonia, and methanol. With no clear consensus on the most effective solution for VLCCs, owners are pursuing a range of propulsion options, leading to a greater variation in newbuilding designs.

In recent years and in the years to come, the drive for decarbonisation measures and regulations has only intensified. Emerging frameworks such as the EU ETS and the IMO’s CII should accelerate the scrapping of older, inefficient vessels, while driving demand for dual-fuel and alternative-fuel-ready newbuilds. The next 25 years will likely see a fragmented but steadily advancing adoption of LNG, methanol, ammonia, and other alternative fuels.

Orderbook and newbuildings

The VLCC orderbook has historically been cyclical. In the early to mid-2000s, surging oil demand from China and the need to build new tankers to transport this extra demand, overwhelmed shipyards and this led to long delivery lead times. This surge was further amplified by OPA90, which required the phase-out of single-hulled tankers in favour of double-hulled designs. As a result, the orderbook-to-fleet ratio climbed above 50%, peaking in 2009 with more than 250 VLCCs on order.

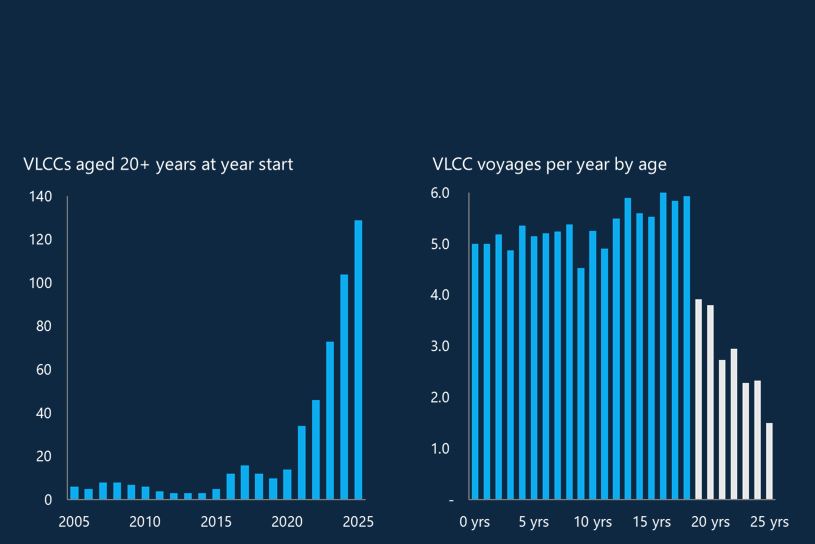

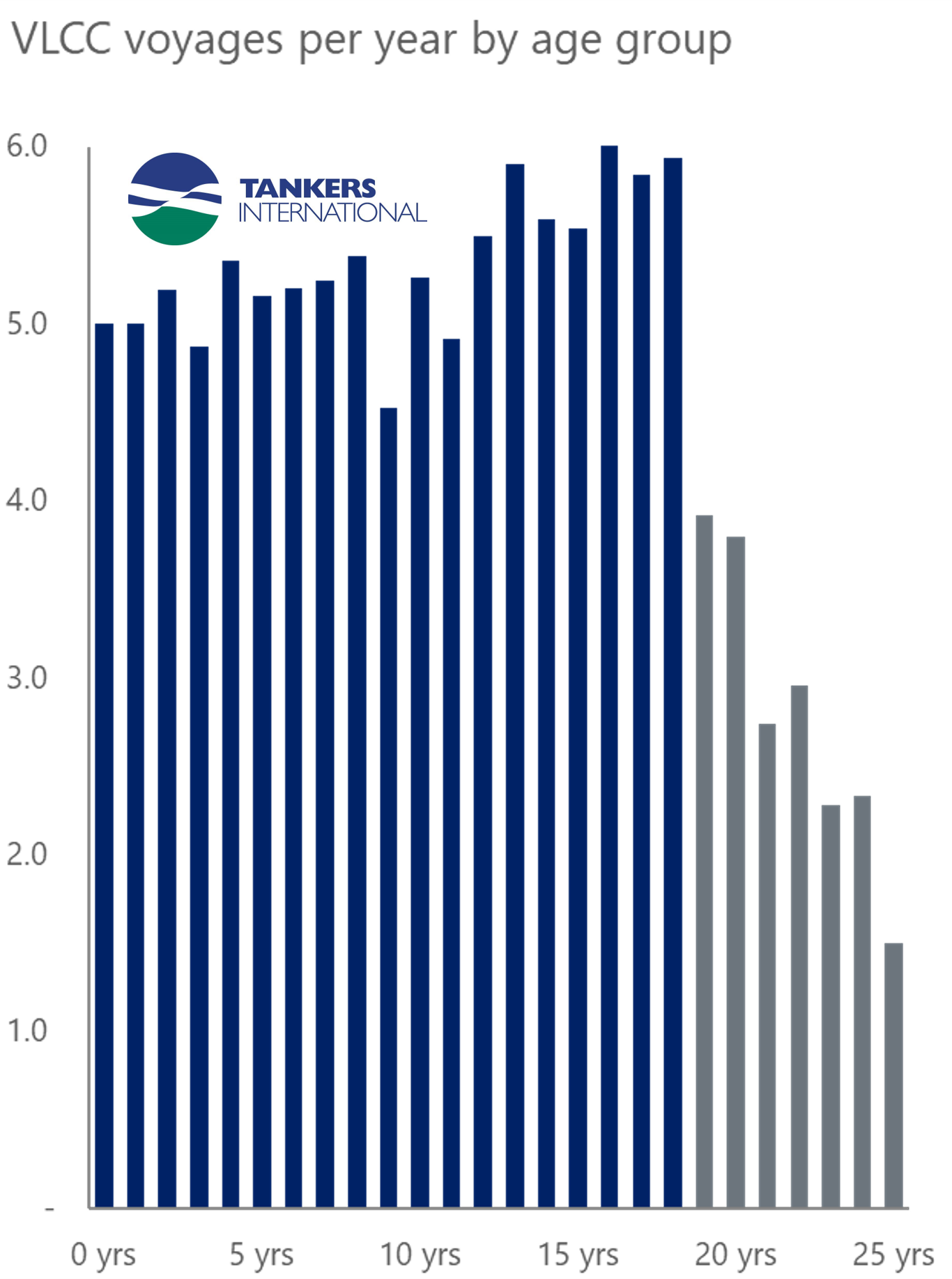

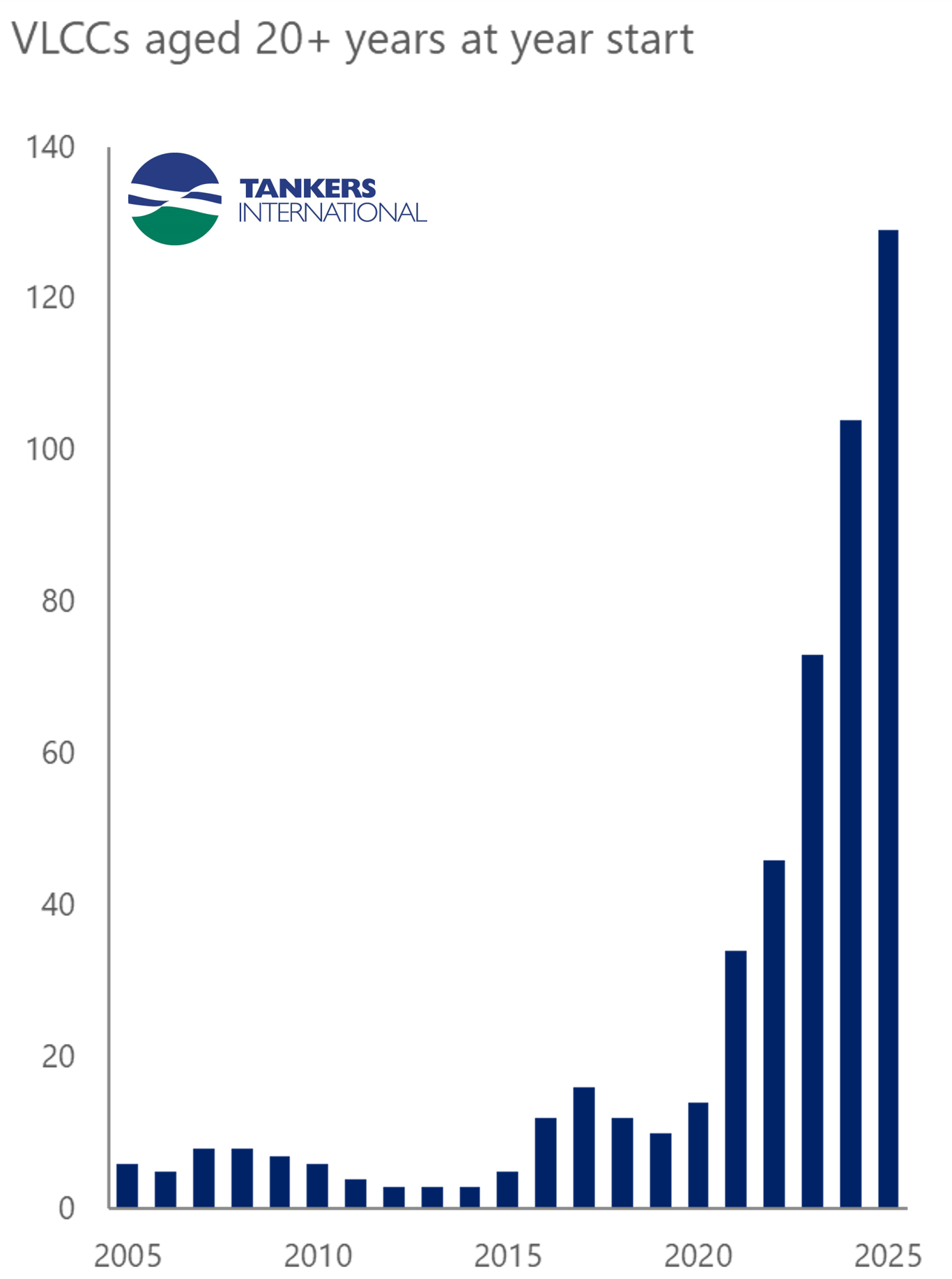

Today, the VLCC market looks very different. Last year, just one single VLCC was delivered, reflecting the industry’s hesitation to commit due to the fuel-transition uncertainty. However, with around 150 VLCCs already over 20 years old, fleet renewal is, once again, unavoidable.

The current orderbook stands at just over 100 vessels, roughly 12% of the trading fleet, and the VLCCs being built today are fundamentally different from their counterparts 25 years ago with optimised hull designs, energy-saving devices, and dual-fuel capabilities, designed not just for efficiency but for flexibility in an era of regulatory uncertainty.

Trade routes: Shift to the east and longer hauls

When Tankers International was formed in 2000, VLCC trade routes looked very different from what they are today, though they have always reflected the geography of oil supply and demand.

In the early 2000s, crude oil flows ran primarily from the Middle East to the US and Europe. Over time, however, the centre of demand shifted decisively eastward.

China’s accession to the World Trade Organization in 2001 triggered a surge in manufacturing and export-led growth, driving a greater demand for crude oil. The resulting economic boom transformed the VLCC market, with tonnemiles climbing as crude moved, not only from the Middle East, but also from West Africa and Latin America to Asia. At the same time, the US shale revolution sharply reduced American oil imports, cutting once-dominant transatlantic flows to a fraction of their former levels.

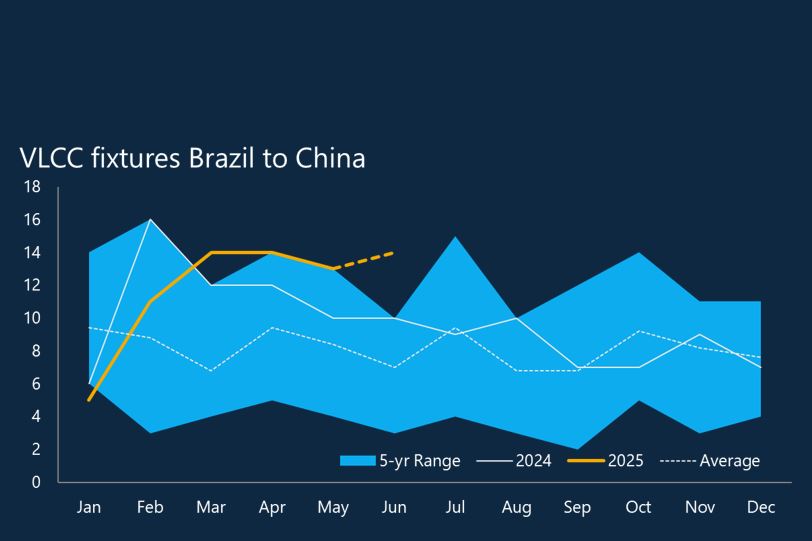

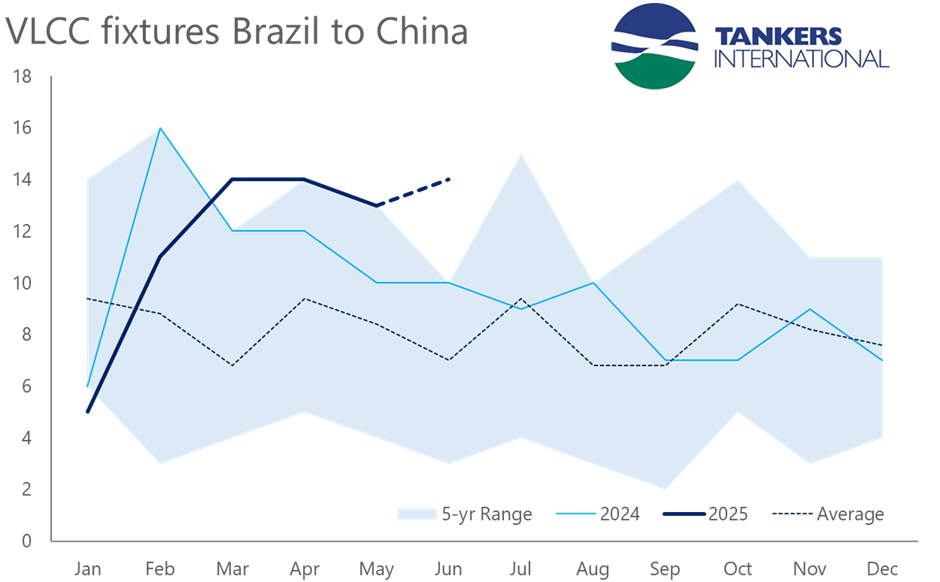

Over the past 25 years, VLCC trade routes have evolved with continued Middle East-to-Asia flows, and now increasing volumes from South America and the US, and long-haul tonnemiles driving demand. As Asian consumption continues to rise and South America emerges as a major supply hub, the eastward momentum is expected to persist, supporting VLCC demand well into the future.

Customers: From oil majors to traders and NOCs

In the early years of the Pool, Western oil majors and NOCs dominated VLCC chartering, often backed by their own fleets. Over time, many oil majors divested their ships and shifted to chartering from independent owners.

Meanwhile, commodity trading houses have emerged as some of the most active and influential charterers, leveraging VLCCs to move cargoes rapidly in pursuit of opportunity trading. NOCs from Asia and the Middle East have also built sophisticated trading arms, seeking greater control over their supply chains.

Looking ahead, new customer types may emerge, the ESG-driven charterers prioritising ‘green’ shipping tonnage on one side, and charterers of sanctioned ‘dark fleet’ tonnage on the other, reflecting the increasingly fragmented market landscape.

Geopolitics and its impact on the market

Geopolitics have always shaped tanker markets, but the risks have evolved. In the early 2000s, concerns centred on Middle Eastern supply disruptions, with events like 9/11 and the Iraq War creating war-risk premiums and sudden spikes in freight rates.

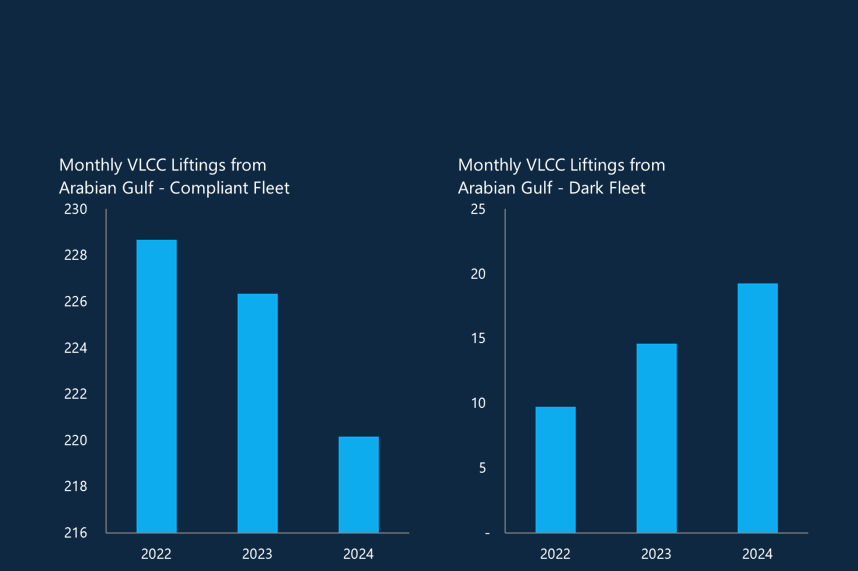

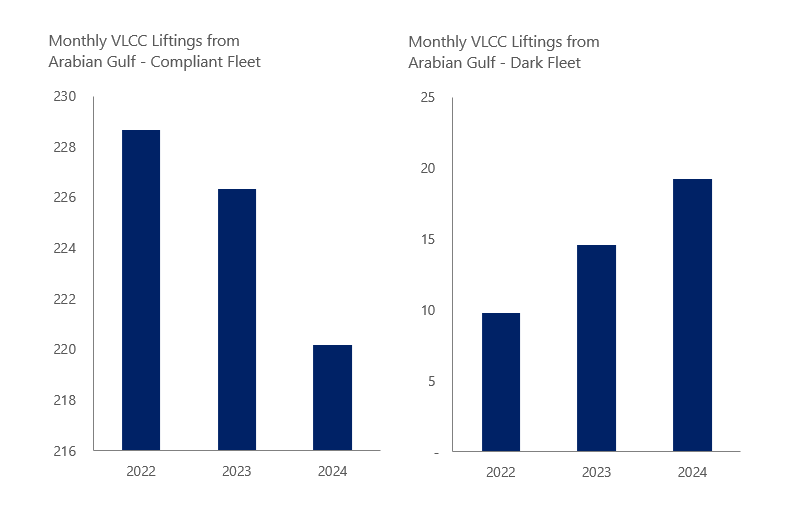

Today, the focus is less on physical supply disruption and more on sanctions and trade fragmentation. The Russia–Ukraine conflict and G7 price cap have re-routed oil flows and spawned a shadow fleet, increasing tonnemiles and reshaping competition.

At the same time, U.S. shale production and growing supply from South America have added supply resilience, diversifying global flows while also creating new geopolitical variables tied to trade policy.

Technology and data

Perhaps the most dramatic change has been the industry’s adoption of technology and data. In 2000, chartering was done by phone and fax, AIS was still in its infancy, and information was fragmented. Market intelligence relied on experience, instinct, and personal networks.

Today, AIS tracking, satellite imagery, and integrated data platforms have made the market almost entirely transparent. Sophisticated analytics guide decisions on routing, congestion, and supply-demand balances, while onboard connectivity has improved communication and seafarer welfare.

Looking forward, Artificial Intelligence (AI) promises even greater optimisation, whether in predictive maintenance, market forecasting, or route planning, while the human element remains essential for negotiation, client relationships, and judgement calls that data alone cannot provide.

The future of the VLCC market

From emerging regulations to trade routes, and the tech boom, the VLCC tanker market has undergone a profound transformation over the past 25 years.

As Tankers International marks its 25th anniversary, one thing is clear, while the challenges facing the VLCC sector continue to evolve, so do the opportunities for innovation and market adaptation, as the industry continues to grow and change.