As the global VLCC community gathers in Dubai for Bahri Week, all eyes are once again on OPEC and Middle East production policy. OPEC+ members, led by Saudi Arabia, have begun unwinding their voluntary production cuts, and the return of supply is reshaping momentum across both oil and tanker markets. After more than a year of orchestrated oil market tightness, the reintroduction of barrels is re-establishing the Middle East as the core driver of VLCC demand.

In oil markets, the balance has shifted subtly but decisively. As Middle Eastern producers have increased output, a growing share of those incremental barrels has been drawn into Asia, which remains the deepest and most price-sensitive demand centre. Earlier this year, Asian refiners relied more on stock drawdowns and opportunistic Atlantic Basin cargoes, but as Middle Eastern supply loosened and differentials softened, their focus has swung back toward to the region.

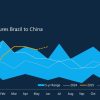

For the tanker market, this evolution has been unambiguously positive. As OPEC+ producers have completed their rebalancing after earlier oversupply and the Middle East moves beyond its seasonal demand peak, more crude oil is now moving into the export market. That is already visible in rising VLCC cargo counts and fixture momentum. The increase has not been dramatic — but it has been consistent and sustainable. It is precisely this kind of predictable, volume-driven trade, rather than sporadic arbitrage flows, that underpins lasting rate support for supertankers.

The VLCC segment remains particularly responsive to Middle East oil flows. With 85% of crude and condensate exported from the region in 2024–2025, already being carried by VLCCs, and 75% of the OPEC+ production increase stemming from this region, the scale of the opportunity is obvious. Each additional barrel made available for export directly translates into greater long-haul transport demand — and VLCCs are uniquely positioned to absorb that trade.

On the supply side, vessel availability remains tight, and with no significant movement in the VLCC fleet size the freight market direction will remain driven by consistent vessel demand in the near term. VLCC fleet growth is effectively negligible this year, with new deliveries limited. Even with more newbuildings scheduled to enter the market in 2026, much of that additional capacity will be offset by an ageing fleet that is gradually seeing its utilisation decline. In practice, the effective reduction in trading ability from older vessels is likely to outweigh the capacity added from new tonnage.

Even with the improving fundamentals, the market is not without risks. Geopolitical volatility in the Middle East and Red Sea remains ever-present and continues to cast a shadow on freight dynamics. The current demand strength also depends on Asian refiners maintaining healthy margins — a downturn there could temper cargo intake. And while OPEC+ is currently prioritising exports, its strategy remains reactive and could pivot back toward restraint if crude prices come under pressure.

Looking ahead, the return of Middle Eastern supply appears to be more than a temporary boost — it signals a structural shift in the fundamentals supporting the VLCC market. With Asia continuing to pull incremental barrels and Middle Eastern exports moving back toward growth rather than restriction, the demand base for VLCCs is strengthening. Combined with limited net fleet expansion and an ageing fleet, the freight market is set to be driven increasingly by cargo demand rather than ship supply. While geopolitical and policy risks remain in view, the balance of momentum has turned decisively positive, and the current strength in the VLCC freight market is a reflection of this shift.