The VLCC freight market has gained momentum in the first half of 2025, with earnings generally higher compared to the latter half of 2024. This improvement comes despite various uncertainties and evolving market dynamics, illustrating the market’s resilience.

One significant driver has been the impact of tariffs, particularly the threat of US tariffs on China. This has led to a decrease in VLCC liftings from the US to China, impacting tonne-miles due to the long-haul nature of this route. In general, VLCC volumes out of the US have declined overall, indicating that American crude oil has been exported on smaller tankers to more localised markets.

The return of OPEC+ voluntary production cuts also played a role in market dynamics. While headline figures point to rising output, much of this increase has been masked by some countries compensating for prior over-production. Additionally, the increase in supply also coincides with regional demand peak in the Middle East. This means we have not seen a significant change in exports from this supply growth. However, mainstream VLCC fixture counts in the Arabian Gulf have shown an upward trend. Looking ahead to the second half of 2025, more barrels will become available for exports as over-producers catch up with targets and seasonal local demand begins to fade.

Sanctioned crude producers, particularly in Iran, continue to disrupt the market. While Iranian exports have been at high levels, the recent escalation of hostilities between Iran and Israel has heightened significant geopolitical risk. Tensions over the Strait of Hormuz, a crucial geopolitical chokepoint, have led to increased insurance premiums and a potential shift in charterer preferences for alternative loading regions. Although the recent ceasefire has brought a measure of stability, the region remains a source of potential volatility for oil flows and tanker operations. Any renewed tensions could be capable of swiftly altering market dynamics.

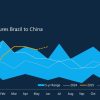

On a more positive note for VLCCs, South America, especially Brazil, has emerged as a significant growth area. Increased crude supply, combined with tightening sanctions on dark fleet tankers and China’s retaliatory tariffs on US crude, has led to a substantial rise in VLCC shipments from Brazil to China. These long-haul voyages are highly supportive of tonne-miles, reinforcing the region’s growing strategic importance in global trade flows.

Global oil demand continues to rise, albeit at a slower pace. China remains a key driver for the VLCC segment, and despite macroeconomic pressure and a slowdown in demand growth, its crude imports have taken an upward trend. There’s a positive sign as China’s refinery maintenance season concludes, potentially leading to more crude oil entering their refining systems. Furthermore, mainstream tanker demand into China has increased, with a notable rise in movements from long-haul load areas like West Africa and South America. Early indications also suggest a decline in sanctioned VLCC trades into China, which could further benefit the mainstream market.

The overall VLCC fleet size remains somewhat inflated due to the continued sales of older vessels to the dark fleet, leading to historically low scrapping rates. However, the orderbook for newbuilds is relatively small. This combined with ongoing oil demand growth, contributes to a generally bullish sentiment for VLCC market microeconomics.

Looking ahead, the VLCC market appears poised for a strong second half of 2025. Geopolitical tensions, notably the Iran-Israel conflict, could continue to drive supply chain disruptions. However, shifting trade patterns due to US tariffs are redirecting long-haul VLCC routes towards growth regions in South America, generating similar valuable tonne-miles. Furthermore, as OPEC+ voluntary production cuts translate into increased actual export volumes, these additional barrels will undoubtedly boost demand for the VLCC segment. Together, these factors indicate a positive trajectory for the VLCC market in the coming months.